Why good cars sometimes trade below their potential value, and why that can still be rational

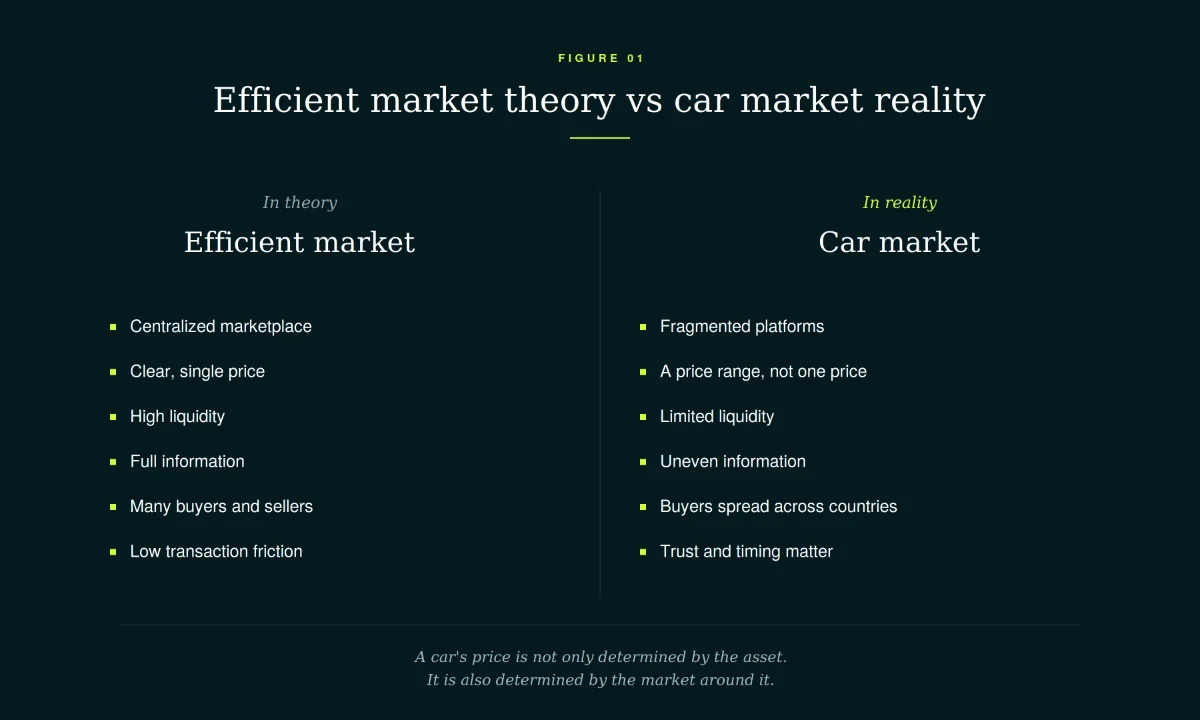

In theory, markets should find the right price. If an asset is underpriced, buyers should compete it up. If it is overpriced, it should not sell. Information should spread, capital should move, and prices should converge.

That is the theory. In reality, especially in cars, price is shaped as much by friction as by value.

A car is not a share of Apple. It does not trade on a centralized exchange with thousands of buyers and sellers visible at the same time. There is no single order book, no instant liquidity, and no perfect market price visible to everyone. Every car is slightly different. Mileage, history, specification, ownership, condition, country of registration, tax position, and presentation all matter. Buyers are spread across platforms, countries, languages, and local markets. Trust is uneven. Information is incomplete. Timing matters.

That is why enthusiast and collector car markets are structurally inefficient. And where inefficiency exists, opportunity can exist. Not only for buyers, but also for sellers.

A car’s price is not only determined by the asset. It is also determined by the market around it.

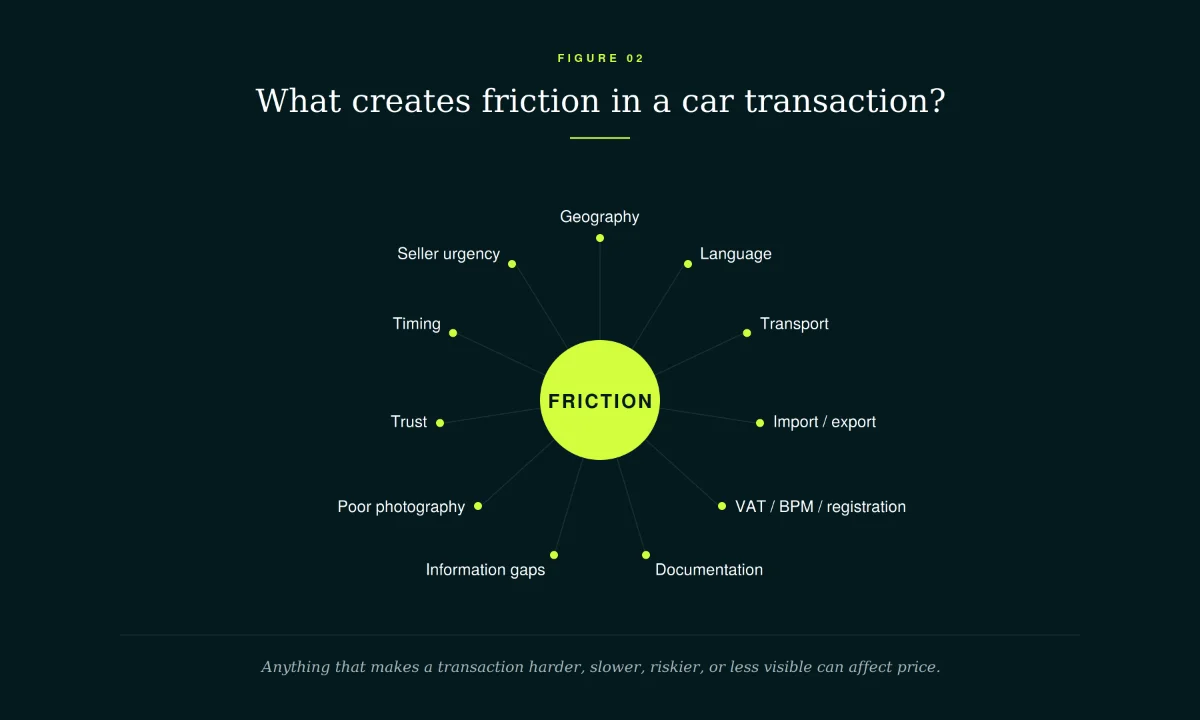

What friction actually is

Friction is anything that makes a transaction harder, slower, riskier, less trusted, or less visible than it should be. In car markets, friction is everywhere.

There is geographic friction: a car may be in another country, far from the buyer. That means transport, distance, language, paperwork, and uncertainty. There is tax and regulatory friction: VAT, BPM, import duties, registration rules, export documents, and uncertainty around the final landed cost can all affect what a buyer is willing to pay.

There is also information friction. A car may have unclear service history, missing invoices, vague ownership details, or a weak description. Presentation friction is related but distinct: poor photos, a lazy listing, no context for the specification, or no proper story can make a good car look average. Trust friction appears when the seller is unfamiliar, the platform is unknown, the paperwork is foreign, or the transaction process feels unclear. Finally, there is liquidity and timing friction: the seller may want to move quickly, while the best buyer may not be actively looking that week.

This is especially visible in Europe. The European enthusiast car market is fragmented across languages, tax systems, registration rules, local platforms, and buyer preferences. A car listed in Belgium may be more attractive to a buyer in the Netherlands, Germany, Denmark, Switzerland, or France than to the local buyer base. But that only matters if the right buyer sees it, understands it, trusts it, and can calculate the transaction properly.

Fragmentation is friction at scale.

Anything that makes a transaction harder, slower, riskier, or less visible can affect price.

Why friction creates price gaps

Friction does not push prices down directly. Friction increases the risk buyers perceive.

When a transaction becomes more complicated, buyers demand compensation. Not necessarily because the car is worse, but because the chance of unexpected costs, administrative issues, delays, incorrect assumptions, or future resale difficulty feels higher.

Take a simple example. A Dutch buyer may be willing to pay €90,000 for a car already registered in the Netherlands, with strong photos, clear documentation, a known history, and a simple transaction process. The same buyer may only be willing to pay €82,000 for a similar car in Italy if they need to arrange transport, verify documents, model the tax outcome, and accept residual uncertainty.

The asset may be similar. The transaction is not. The €8,000 difference does not necessarily mean the market is being irrational. It is the market applying a discount for risk, uncertainty, complexity, and effort.

This is closely related to how illiquidity works in finance. Assets that are harder to trade often trade at a discount because buyers demand compensation for the risk, uncertainty, and work they take on. Some of the best opportunities in financial markets appear where the asset is good, but the transaction is difficult. Distressed assets, illiquid securities, or physical commodities in the wrong place at the wrong time can trade below theoretical value because not every buyer is able or willing to solve the complexity.

The same principle applies to cars. A good car with poor photos may be overlooked. A rare specification may be described badly. A foreign-registered car may scare away casual buyers. A seller may want to move quickly. A car may have paperwork questions that are real, but solvable. An export or import angle may be misunderstood by the local market.

That is where the buyer's edge appears. The opportunity is not that the market is wrong for no reason. The opportunity is that the market may overprice the risk behind the friction.

Consider a real example.

A 2016 Rolls-Royce Wraith: original spec, 49,000 km, fully documented, sold via auction at €120,123 to a buyer willing to handle the cross-border transaction from Lithuania. Comparable cars sit on listing platforms in Western Europe at €180,000 to €195,000, though those are asking prices rather than transaction prices. The cars are similar. The transactions are not. The buyer earned the difference by being willing to do what the broader market would not: pay attention to a smaller local market, evaluate Lithuanian paperwork, arrange transport.

That is the buyer's edge in real numbers. It is also the question the next section has to answer: why would any rational seller accept it?

The car did not change. The transaction did.

The car did not change. The transaction did.

Why sellers can rationally accept that discount

At first, this seems like a contradiction. If buyers can benefit from buying below theoretical value, how can sellers also benefit?

The answer is that sellers are not always maximizing theoretical price. They are maximizing utility. Utility includes time, certainty, liquidity, effort, risk, and opportunity cost.

A seller may rationally accept €90,000 today instead of holding out for a possible €93,000 in six months. That does not mean the seller is irrational. They may need liquidity now. They may want to fund a business. They may want to buy another car. They may have a better investment opportunity. They may value certainty over a long and uncertain private-sale process.

Six months of viewings, low offers, failed buyers, financing issues, trade-in requests, depreciation and negotiation has a cost. The finance concept here is opportunity cost. Cash today is not the same as cash later. A higher future price is only better if the waiting period, uncertainty, effort, and risk are free. They usually are not.

The €3,000 “left on the table” is only left there if you assume the alternative was costless. It rarely is. If the seller can use the capital elsewhere, or if certainty has more value than waiting, accepting a discount may be the rational decision.

That is why a transaction can make sense for both sides. The buyer is paid for absorbing friction. The seller is paid in liquidity, certainty, and time.

A transaction can make sense for both sides when each side values time, risk, liquidity, and effort differently.

Information asymmetry, and how sellers close the gap

Friction is not only about geography or paperwork. It is also about information.

When buyers cannot verify quality, they discount the car. They do not only discount bad cars. They discount uncertainty. That is the difficult part for honest sellers. A good car with weak presentation can be punished in the same way as a bad car with weak presentation, because the buyer cannot easily tell the difference from a thumbnail, a short description, or a few unclear photos.

In economics, this is the basic problem of information asymmetry. One side knows more than the other. The seller knows the car. The buyer sees only what is made visible.

So the seller’s job is not simply to claim the car is good. It is to make quality as easy as possible for the buyer to verify.

That means photography that actually shows the car. Complete service history, presented clearly, not just claimed. Honest condition reporting, including flaws. Clear ownership and documentation. Accurate specification and option details. A transparent process. A realistic reserve. A genuine narrative around what the car is, who it was built for, and why this particular example matters.

This is not cosmetic. Presentation changes confidence, and confidence affects price. Reducing friction does not change the car. It changes how confidently the market can value it.

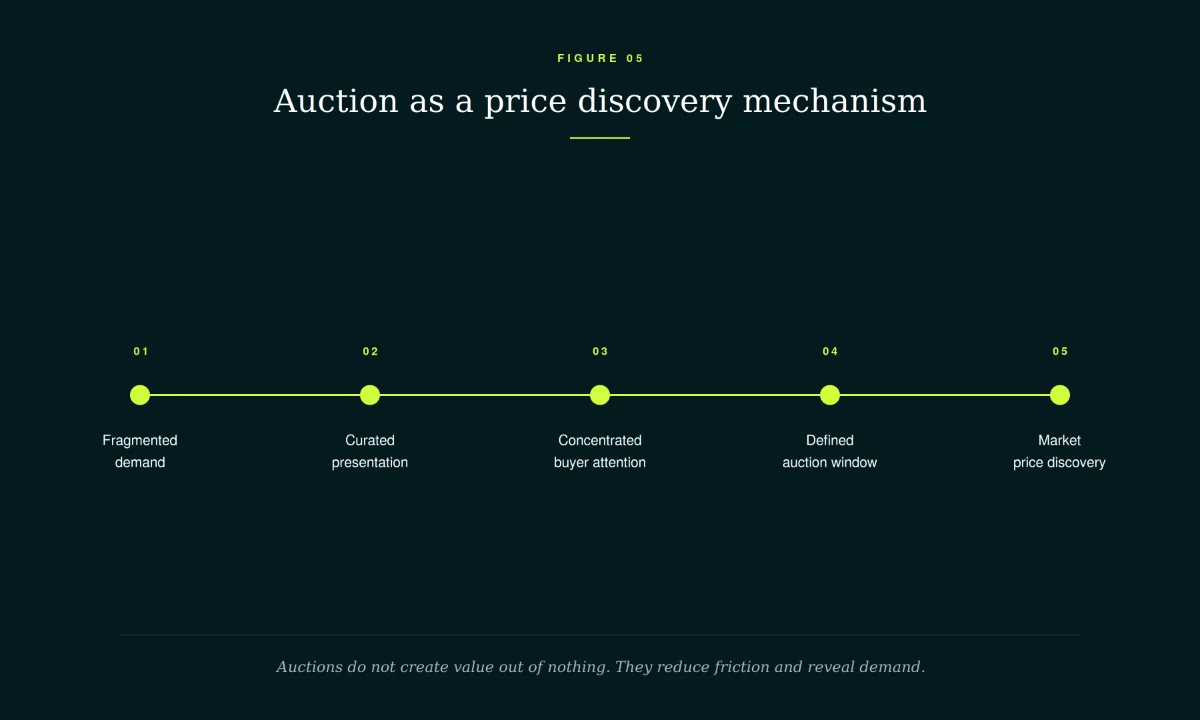

Auctions as a friction-reducing mechanism

An auction is not magic. It does not guarantee the highest imaginable price. It does not make every reserve realistic. It does not turn a weak market into a strong one.

But an auction can reduce specific frictions. It concentrates demand into a defined window. It makes interest visible. It can turn passive watchers into active bidders. It replaces open-ended negotiation with a deadline. It reveals real demand against a reserve, instead of relying only on asking prices.

That matters because asking prices are not transaction prices. A car listed privately for €100,000 has not necessarily been valued by the market at €100,000. It has only been offered at that level. The real question is whether a serious buyer is willing to execute at that price.

An auction answers a different question: what is the market willing to pay within a defined window?

That is price discovery.

At Octane, this is how we think about the role of auctions in the enthusiast car market. The goal is not to pretend that every car is worth more at auction. The goal is to reduce friction where possible: better presentation, clearer information, broader reach, a concentrated buyer pool, and a transparent process.

Auctions do not create value out of nothing. They reduce certain frictions and reveal demand.

Price discovery is not about creating value. It is about revealing demand.

Inefficiency is the opportunity

Inefficiency in the enthusiast car market is not necessarily a flaw to be fixed. It is a structural feature of trading physical, unique, cross-border assets between human beings who each value time, risk, effort, and capital differently.

For buyers, opportunity exists where the market has overpriced the risk behind the friction. A car may be better than its photos. A specification may be undersold. A foreign-registered car may look complicated to most buyers but straightforward to someone who knows the process. A seller may want speed and certainty more than the highest theoretical bid.

For sellers, opportunity exists in reducing friction. Better information, better presentation, clearer documentation, and access to a wider buyer pool can move a car closer to its best executable market value. Not because the car itself has changed, but because the market’s confidence in the car has changed.

Both can be true at once because each side is solving a different problem. The buyer is solving complexity. The seller is solving liquidity, timing, trust, and market access.

That is why inefficient markets reward careful analysis. In a perfectly efficient market, there is little room to see what others have missed. In an inefficient market, preparation, information, trust and timing matter.

The buyer is rewarded for estimating risk better. The seller is rewarded for reducing friction.

That is not a contradiction.

That is how transactions in inefficient markets come together.